Mid Term Part (2): Individual Assignment: Tornado Diagrams and Bidding¶

By: Chengyi (Jeff) Chen

%load_ext autotime

%load_ext nb_black

%matplotlib inline

%config InlineBackend.figure_format = 'retina'

# Graphing

import matplotlib.pyplot as plt

import seaborn as sns

# Plotting Design Configs

sns.set(

font="Verdana",

rc={

"axes.axisbelow": False,

"axes.edgecolor": "lightgrey",

"axes.facecolor": "None",

"axes.grid": True,

"grid.color": "lightgrey",

"axes.labelcolor": "dimgrey",

"axes.spines.right": False,

"axes.spines.top": False,

"figure.facecolor": "white",

"lines.solid_capstyle": "round",

"patch.edgecolor": "w",

"patch.force_edgecolor": True,

"text.color": "dimgrey",

"xtick.bottom": False,

"xtick.color": "dimgrey",

"xtick.direction": "out",

"xtick.top": False,

"ytick.color": "dimgrey",

"ytick.direction": "out",

"ytick.left": False,

"ytick.right": False,

"figure.dpi": 100,

"figure.figsize": (8, 6),

},

)

sns.set_context(

"notebook", rc={"font.size": 10, "axes.titlesize": 12, "axes.labelsize": 10}

)

sns.color_palette(palette="Spectral")

# General

import numpy as np

import scipy.stats as sp

import pandas as pd

from functools import partial

# Ignore warnings LOL

import warnings

warnings.simplefilter("ignore")

time: 1.22 s (started: 2021-04-02 15:44:56 +08:00)

def ρ(γ):

"""Risk tolerance"""

return 1 / γ

time: 302 µs (started: 2021-04-02 15:44:57 +08:00)

def r(γ):

"""Risk Odds"""

return np.log(γ)

time: 414 µs (started: 2021-04-02 15:44:57 +08:00)

def u(x, γ: np.array = np.array([0.0]), a: float = 0.0, b: float = 1.0):

"""Assuming user satisifies the Δ property,

calculates the U-values using either a

Piecewise Linear u = a + bx if γ = 0 (Risk-Neutral)

else Exponential u = a + be^(-xγ) U-curve U(x)

Args:

x (np.array): Payoffs of prospects matrix, Shape = (Number of deals, Number of prospects in each deal)

γ (np.array): Risk-aversion coefficients, Shape = (Number of different risk-aversion coefficients for sensitivity analysis), Default = 0.0 (Risk-neutral) [γ > 0: Risk-averse, γ < 0: Risk-seeking]

a (float): Constant for U-curve

b (float): Coefficient for payoff variable

Returns:

np.array:

U-values, Shape = (Number of Risk Aversion Coefficients γ, Number of deals, Number of prospects in each deal)

"""

assert (

x.ndim == 2

), "Payoffs require 2 dimensions, first dim is number of deals, second is number of prospects in each deal."

γ = np.array([γ]) if np.isscalar(γ) else np.array(γ)

return np.array(

[

np.apply_along_axis(

func1d=lambda x, γ=γ: a + b * x if γ == 0 else a + b * np.exp(-x * γ),

axis=-1,

arr=x,

γ=γ_i,

)

for γ_i in γ

]

)

time: 627 µs (started: 2021-04-02 15:44:57 +08:00)

def eu(u, p):

"""Assuming user satisifies the Δ property, calculates the

hadamard product of the u values matrix and probabilities

matrix (respective probabilities associated with each

prospect in the u matrix)

Args:

u (np.array): U-values matrix, Shape = (Number of Risk Aversion Coefficients γ, Number of deals, Number of prospects in each deal)

p (np.array): Probabilities of each prospect matrix, Shape = (Number of Risk Aversion Coefficients γ, Number of deals, Number of prospects in each deal)

Returns:

np.array:

E-values, Shape = (Number of Risk Aversion Coefficients γ, Number of deals)

"""

assert (

u.shape == p.shape

), "U-values matrix must be the same shape as the probabilities matrix."

assert (

u.ndim == 3

), "Both matrices must have 3 dimensions, Shape = (Number of Risk Aversion Coefficients γ, Number of deals, Number of prospects in each deal)."

return np.sum(u * p, axis=-1)

time: 545 µs (started: 2021-04-02 15:44:57 +08:00)

def u_inv(eu, γ: np.array = np.array([0.0]), a: float = 0, b: float = 1):

"""Piecewise Inverse of Linear if γ = 0 (Risk-Neutral)

else Inverse of Exponential U-curve Certain equivalent

function U^{-1}(x)

Args:

eu (np.array): E[U-Values] / Expectation over u-values, AKA E-values, Shape = (Number of Risk Aversion Coefficients γ, Number of deals)

γ (np.array): Risk-aversion coefficients, Shape = (Number of different risk-aversion coefficients for sensitivity analysis), Default = 0.0 (Risk-neutral) [γ > 0: Risk-averse, γ < 0: Risk-seeking]

a (float): Constant for U-curve

b (float): Coefficient for payoff variable

Returns:

np.array:

Certainty Equivalent values, Shape = (Number of Risk Aversion Coefficients γ, Number of deals)

"""

γ = np.array([γ]) if np.isscalar(γ) else np.array(γ)

for eu_i, γ_i in zip(eu, γ):

if not np.isclose(γ_i, 0):

assert np.alltrue(

eu_i > 0

), "E[U-Values] / Expectation over u-values must be positive for γ > 0 and γ < 0 in order for inverse of Exponential U-curve to work."

assert (

eu.shape[0] == γ.shape[0]

), "E-values first dimension must be the same as γ first dimension for inverse operation."

return np.array(

[

list(

map(

lambda eu, γ=γ_i: (eu - a) / b if γ == 0 else -(1 / γ) * np.log(eu),

eu_i,

)

)

for eu_i, γ_i in zip(eu, γ)

]

)

time: 839 µs (started: 2021-04-02 15:44:57 +08:00)

def certainty_equivalent_values_calculator(

u,

u_inv,

x: np.array = None,

p: np.array = None,

N: int = 10,

payout_lb: float = 0.0,

payout_ub: float = 100.0,

γ: np.array = np.array([0.0]),

):

"""Assuming user satisifies the Δ property, calculates the Certainty Equivalent values for a given

payoff matrix `x` and probability matrix `p`. If both matrices

are not provided, random matrices will be sampled to simulate

calculations.

Args:

u (function): U-curve function

u_inv (function): Inverse U-curve function

x (np.array): Payoffs of prospects matrix, Shape = (Number of deals, Number of prospects in each deal)

p (np.array): Probabilities of each prospect matrix, Shape = (Number of deals, Number of prospects in each deal)

N (int): Number of prospects

payout_lb (float): Lower Bound of Payout for simulation, Default = 0.0

payout_ub (float): Upper Bound of Payout for simulation, Default = 100.0

γ (np.array): Risk-aversion coefficients, Shape = (Number of different risk-aversion coefficients for sensitivity analysis), Default = 0.0 (Risk-neutral) [γ > 0: Risk-averse, γ < 0: Risk-seeking]

Returns:

np.array:

Certainty Equivalent values, Shape = (Number of Risk Aversion Coefficients γ, Number of deals)

"""

γ = np.array([γ]) if np.isscalar(γ) else np.array(γ)

# Case 1: Simulator - Both x and p arent provided

if p is None and x is None:

# Preferential probabilities for each prospect

p = np.random.dirichlet(np.ones(N), size=1)

# Payouts for each prospect

x = np.expand_dims(np.random.randint(payout_lb, payout_ub, size=N), axis=0)

# Case 2: Simulator - Only payouts provided

elif p is None:

# Payouts for each prospect

x = np.expand_dims(

np.random.randint(payout_lb, payout_ub, size=p.shape[-1]), axis=0

)

# Case 3: Simulator - Only probabilities provided

elif x is None:

# Preferential probabilities for each prospect

p = np.random.dirichlet(np.ones(x.shape[-1]), size=1)

# Case 4: Calculator - Both are provided

else:

pass

# Check that payoffs and probability assignments are the same shape

assert (

x.shape == p.shape

), "Payoffs `x` and Probabilities `p` must be the same shape=(Number of deals, Number of prospects in each deal)."

# Calculates U-values Shape = (Number of Risk Aversion Coefficients γ, Number of deals, Number of prospects in each deal)

u_values = u(x, γ=γ)

# Reshape p to match U-values shape

p_reshaped = np.array([p for _ in range(u_values.shape[0])])

# Expectation of U values Shape = (Number of Risk Aversion Coefficients γ, Number of deals)

eu_values = eu(u=u_values, p=p_reshaped)

# Certainty equivalent value of deal

ce_values = u_inv(eu_values, γ=γ)

return ce_values

time: 1.23 ms (started: 2021-04-02 15:44:57 +08:00)

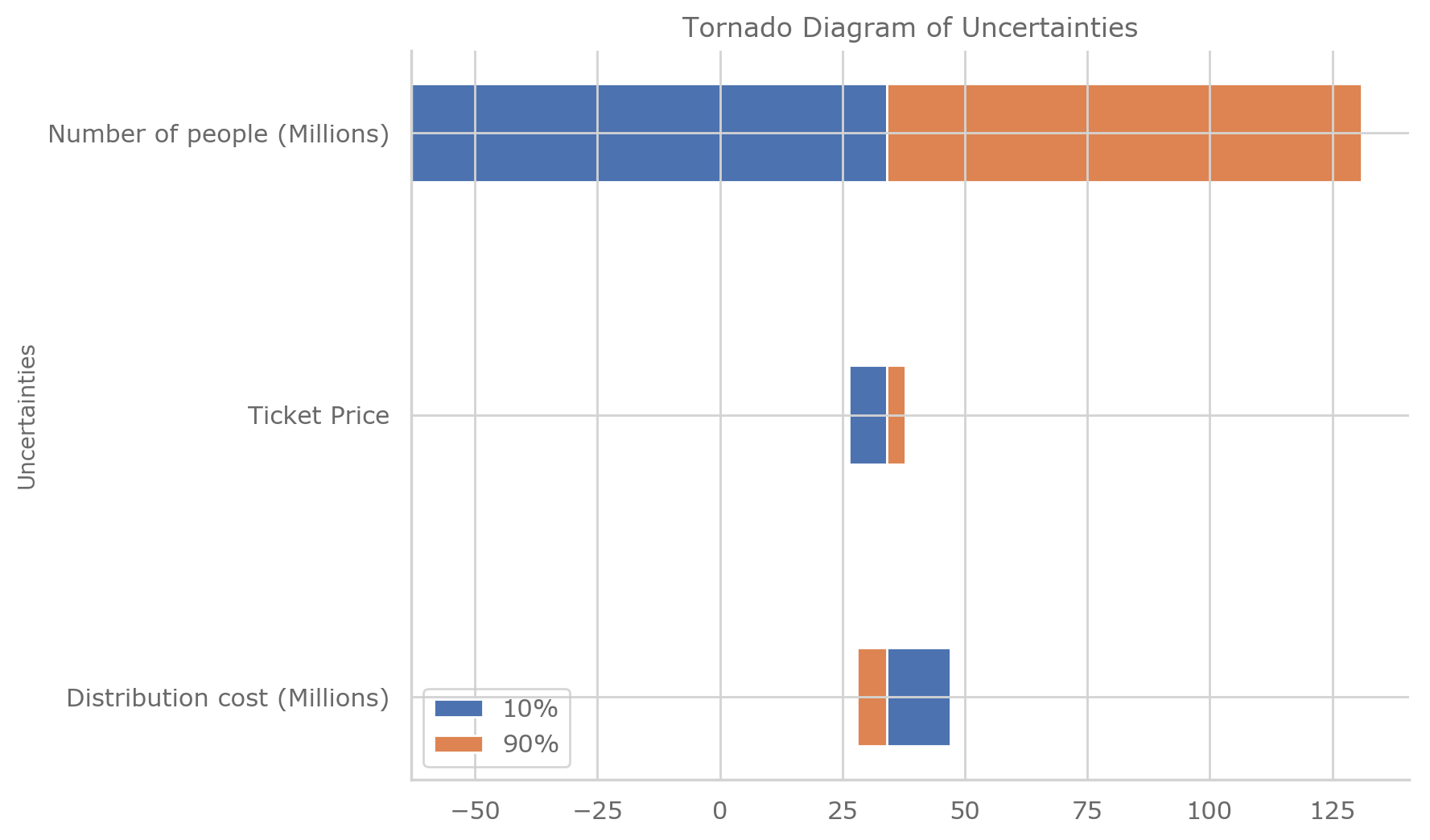

1) Tornado Diagrams: The Clairvoyant goes to College¶

Flicks Inc is a major entertainment corporation. They have just produced a major motion picture called The Clairvoyant goes to College. They have spent some money on the movie and they believe their future profit is calculated as

They provide the following 10-50-90 assessments for three uncertainties. (Distribution cost and Number people seeing movie is in millions of \(\$ \) while ticket price is in \(\$ \))

Draw the tornado diagram and show all tables used in the calculations.

clairvoyant_goes_to_college_uncertainties = pd.DataFrame(

data=[[11.33, 76.0, 140.66], [7.0, 7.5, 7.75], [67.0, 80.0, 86.0]],

index=[

"Number of people (Millions)",

"Ticket Price",

"Distribution cost (Millions)",

],

columns=["10%", "50%", "90%"],

)

clairvoyant_goes_to_college_uncertainties

| 10% | 50% | 90% | |

|---|---|---|---|

| Number of people (Millions) | 11.33 | 76.0 | 140.66 |

| Ticket Price | 7.00 | 7.5 | 7.75 |

| Distribution cost (Millions) | 67.00 | 80.0 | 86.00 |

time: 10.3 ms (started: 2021-04-02 15:44:57 +08:00)

# Profit Formula (Millions)

profit = lambda n_ppl, ticket_px, dist_cost: (0.2 * n_ppl * ticket_px) - dist_cost

time: 370 µs (started: 2021-04-02 15:44:57 +08:00)

# Get the Profit, fixing entries and using baseline (50%) values as other parameters

npv = clairvoyant_goes_to_college_uncertainties.copy()

for row in clairvoyant_goes_to_college_uncertainties.index:

for col in clairvoyant_goes_to_college_uncertainties.columns:

profit_params = clairvoyant_goes_to_college_uncertainties["50%"].copy()

profit_params[row] = clairvoyant_goes_to_college_uncertainties[col][row]

npv[col][row] = profit(*profit_params)

npv

| 10% | 50% | 90% | |

|---|---|---|---|

| Number of people (Millions) | -63.005 | 34.0 | 130.99 |

| Ticket Price | 26.400 | 34.0 | 37.80 |

| Distribution cost (Millions) | 47.000 | 34.0 | 28.00 |

time: 10.1 ms (started: 2021-04-02 15:44:57 +08:00)

# Max Swing

max_swing = npv.max(axis=1) - npv.min(axis=1)

max_swing

Number of people (Millions) 193.995

Ticket Price 11.400

Distribution cost (Millions) 19.000

dtype: float64

time: 6.65 ms (started: 2021-04-02 15:44:57 +08:00)

# Max Swing Squared

max_swing_squared = max_swing ** 2

max_swing_squared

Number of people (Millions) 37634.060025

Ticket Price 129.960000

Distribution cost (Millions) 361.000000

dtype: float64

time: 2.8 ms (started: 2021-04-02 15:44:57 +08:00)

# Normalized Max Swing Squared

norm_max_swing_squared = max_swing_squared / sum(max_swing_squared)

norm_max_swing_squared

Number of people (Millions) 0.987122

Ticket Price 0.003409

Distribution cost (Millions) 0.009469

dtype: float64

time: 3.32 ms (started: 2021-04-02 15:44:57 +08:00)

# Tornado diagram

npv = npv.reindex(norm_max_swing_squared.index[::-1])

fig, ax = plt.subplots()

ax.barh(

npv.index,

npv["50%"].values - npv["10%"].values,

0.35,

align="center",

label="10%",

left=npv["10%"].values,

)

ax.barh(

npv.index,

npv["90%"].values - npv["50%"].values,

0.35,

align="center",

label="90%",

left=npv["50%"].values,

)

ax.set_ylabel("Uncertainties")

ax.set_title("Tornado Diagram of Uncertainties")

ax.legend()

plt.show()

time: 311 ms (started: 2021-04-02 15:44:57 +08:00)

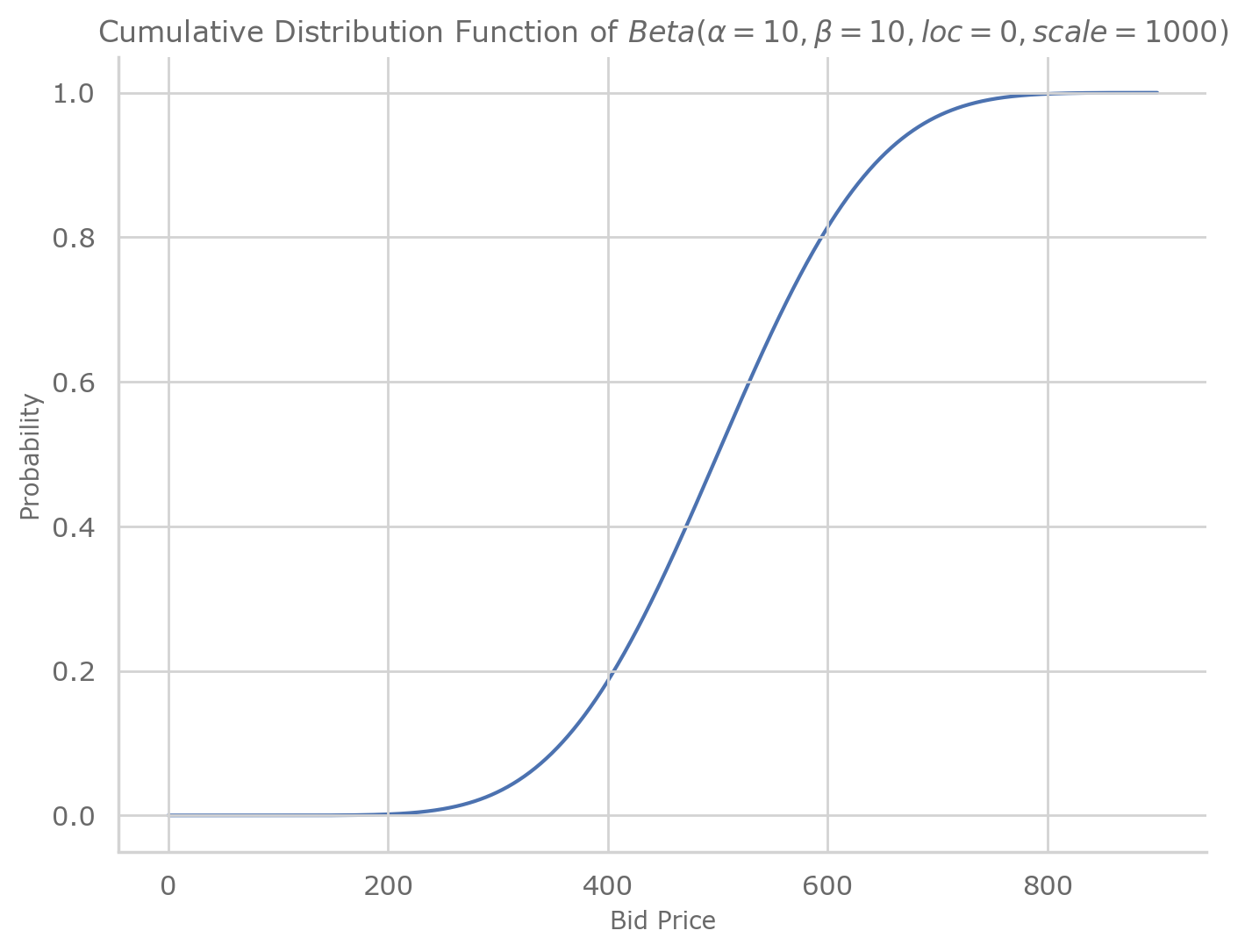

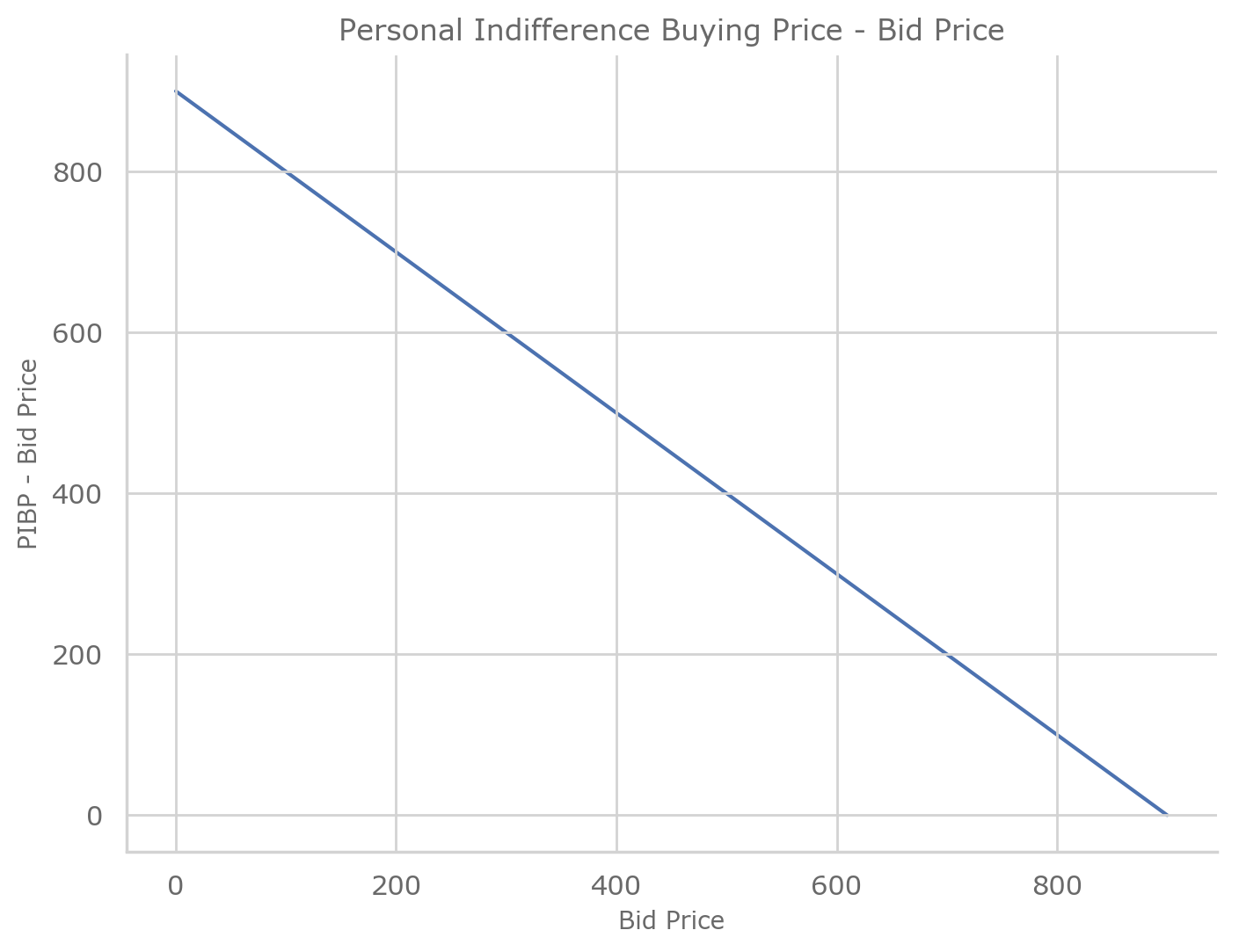

2) Optimal Bidding¶

Determine the optimal bid for a decision maker with an exponential \(u\)-function with a risk aversion coefficient, \(\gamma = 0.001\), a maximum competitive bid distribution, as a scaled Beta distribution, \(Beta\left(\alpha=10, \beta=10, \text{loc}=0, \text{scale}=1000\right)\), and PIBP for the bidding item is \( \$ 900\).

Plot the Opposing forces of bidding (i.e. plot the CDF and the curve of [PIBP-bid])

pibp = 900

γ = 0.001

bids = np.array(list(range(900 + 1)))

pibp_net = pibp - bids

p_acquire = np.array([sp.beta.cdf(x=rv, a=10, b=10, loc=0, scale=1000) for rv in bids])

time: 202 ms (started: 2021-04-02 15:44:58 +08:00)

fig, ax = plt.subplots(1, 1)

ax.plot(bids, p_acquire)

ax.set_xlabel("Bid Price")

ax.set_ylabel("Probability")

ax.set_title(

r"Cumulative Distribution Function of $Beta \left(\alpha=10, \beta=10, loc=0, scale=1000 \right)$"

)

plt.show()

time: 483 ms (started: 2021-04-02 15:44:58 +08:00)

fig, ax = plt.subplots(1, 1)

ax.plot(bids, pibp_net)

ax.set_xlabel("Bid Price")

ax.set_ylabel("PIBP - Bid Price")

ax.set_title(r"Personal Indifference Buying Price - Bid Price")

plt.show()

time: 271 ms (started: 2021-04-02 15:44:58 +08:00)

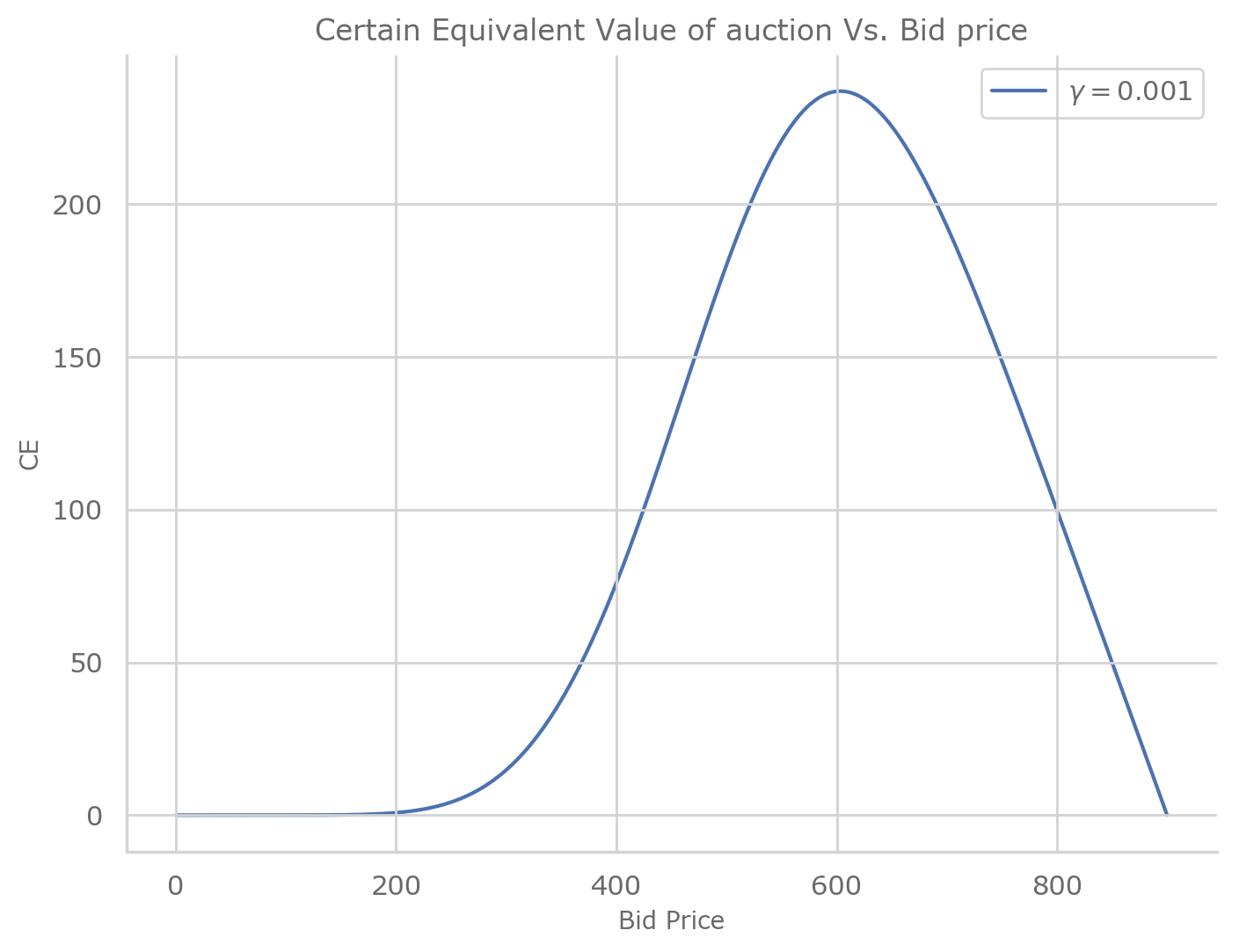

Plot the value of the auction situation (certain equivalent) vs the bid amount.

fig, ax = plt.subplots(1, 1)

ax.plot(

bids,

certainty_equivalent_values_calculator(

u=partial(u, γ=np.array([γ]), a=0, b=1),

u_inv=partial(u_inv, γ=np.array([γ]), a=0, b=1),

x=np.vstack((pibp_net, np.zeros(pibp_net.shape))).T,

p=np.vstack((p_acquire, 1 - p_acquire)).T,

γ=np.array([γ]),

)[0],

label=r"$\gamma = 0.001$",

)

ax.set_xlabel("Bid Price")

ax.set_ylabel("CE")

ax.set_title(r"Certain Equivalent Value of auction Vs. Bid price")

plt.legend()

plt.show()

time: 293 ms (started: 2021-04-02 15:44:59 +08:00)

Determine the least amount the decision maker needs to be paid in order to not participate in this bidding situation.

certainty_equivalent_auction_values = np.round(

certainty_equivalent_values_calculator(

u=partial(u, γ=0.001, a=0, b=1),

u_inv=partial(u_inv, γ=0.001, a=0, b=1),

x=np.vstack((pibp_net, np.zeros(pibp_net.shape))).T,

p=np.vstack((p_acquire, 1 - p_acquire)).T,

γ=0.001,

)[0],

2,

)

print(

"The minimum amount the decision maker needs to be paid in order to not participate in the bidding is: ${}".format(

np.min(

certainty_equivalent_auction_values[

np.nonzero(certainty_equivalent_auction_values)

]

)

)

)

The minimum amount the decision maker needs to be paid in order to not participate in the bidding is: $0.01

time: 15.8 ms (started: 2021-04-02 15:44:59 +08:00)

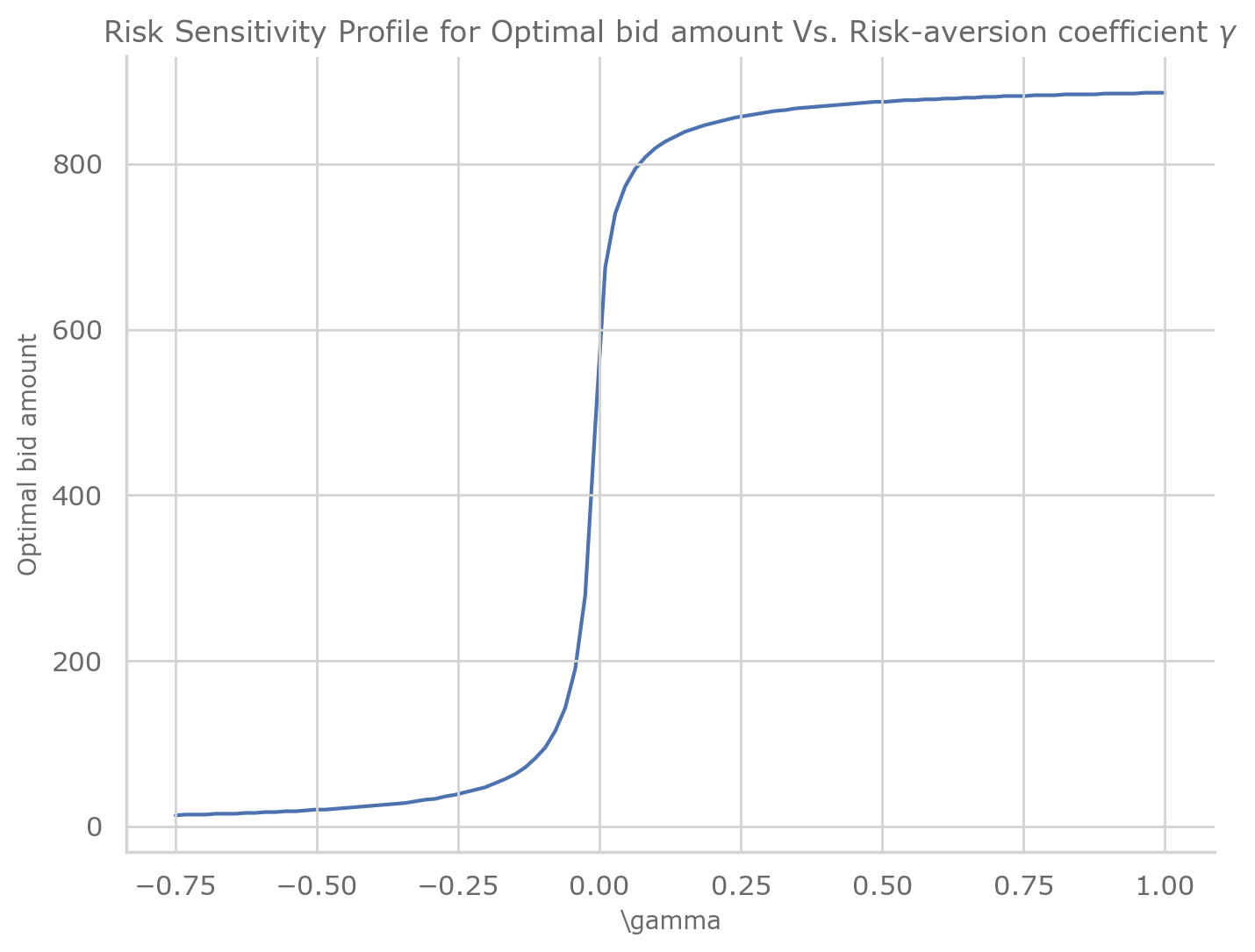

Plot a sensitivity analysis for the optimal bid vs. the risk aversion coefficient.

fig, ax = plt.subplots(1, 1)

γ = np.linspace(-0.75, 1, num=100)

ax.plot(

γ,

[

bids[optimal_bid_idx_for_γ]

for optimal_bid_idx_for_γ in np.argmax(

certainty_equivalent_values_calculator(

u=partial(u, γ=γ, a=0, b=1),

u_inv=partial(u_inv, γ=γ, a=0, b=1),

x=np.vstack((pibp_net, np.zeros(pibp_net.shape))).T,

p=np.vstack((p_acquire, 1 - p_acquire)).T,

γ=γ,

),

axis=1,

)

],

)

ax.set_xlabel(r"\gamma")

ax.set_ylabel("Optimal bid amount")

ax.set_title(

r"Risk Sensitivity Profile for Optimal bid amount Vs. Risk-aversion coefficient $\gamma$"

)

plt.show()

time: 1.13 s (started: 2021-04-02 15:44:59 +08:00)

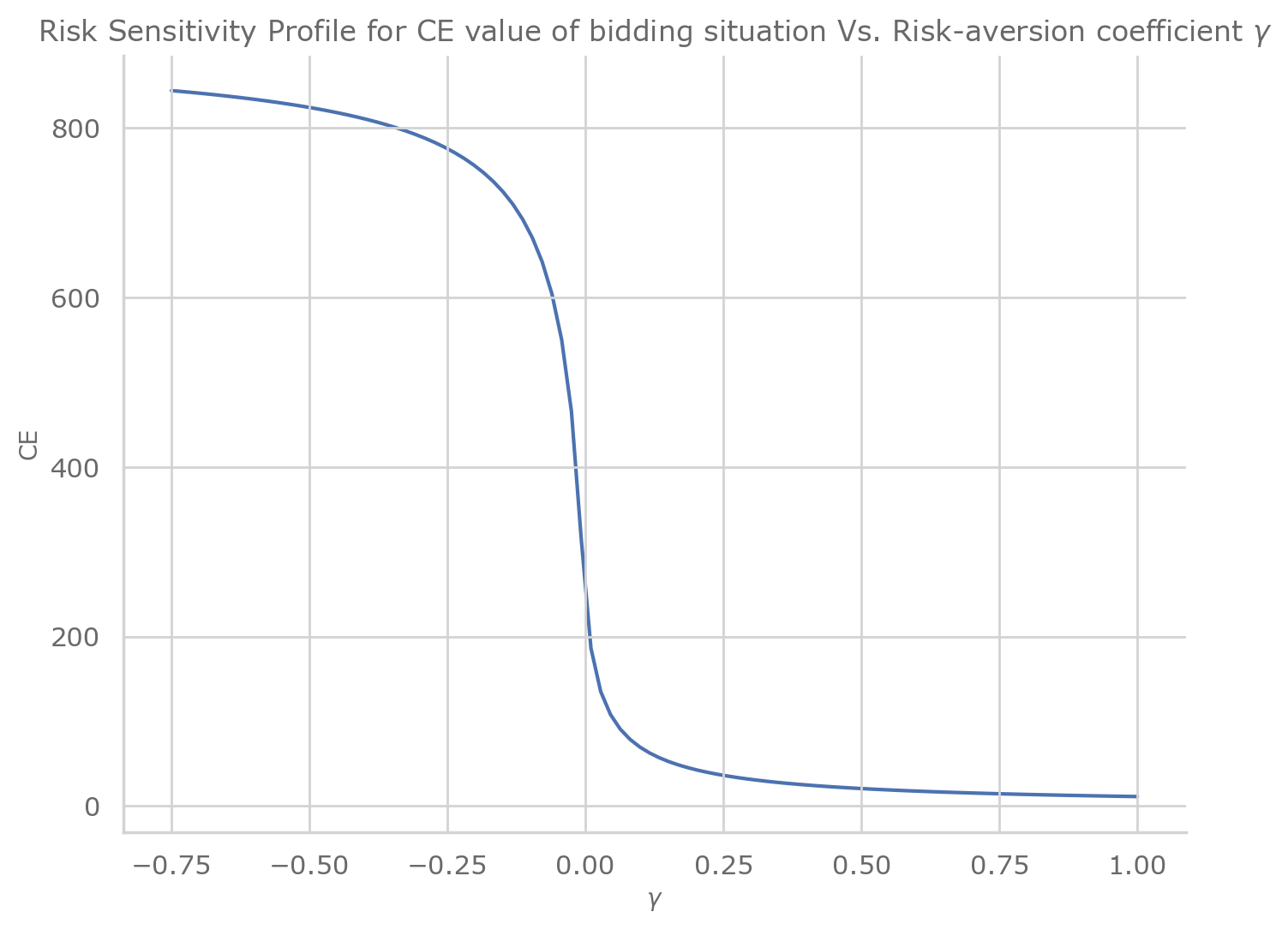

Plot a sensitivity analysis for value of bidding situation vs the risk aversion coefficient.

fig, ax = plt.subplots(1, 1)

γ = np.linspace(-0.75, 1, num=100)

ax.plot(

γ,

np.max(

certainty_equivalent_values_calculator(

u=partial(u, γ=γ, a=0, b=1),

u_inv=partial(u_inv, γ=γ, a=0, b=1),

x=np.vstack((pibp_net, np.zeros(pibp_net.shape))).T,

p=np.vstack((p_acquire, 1 - p_acquire)).T,

γ=γ,

),

axis=1,

),

)

ax.set_xlabel(r"$\gamma$")

ax.set_ylabel("CE")

ax.set_title(

"Risk Sensitivity Profile for CE value of bidding situation Vs. Risk-aversion coefficient $\gamma$"

)

plt.show()

time: 997 ms (started: 2021-04-02 15:45:00 +08:00)

Extra Credit: Plot a two-way sensitivity analysis for optimal bid vs the two parameters (risk aversion coefficient and PIBP). This is a 3D plot.

from mpl_toolkits.mplot3d import Axes3D

from matplotlib import cm, colors

from matplotlib.ticker import LinearLocator

fig, ax = plt.subplots(subplot_kw={"projection": "3d"})

bids = np.array(list(range(900 + 1)))

p_acquire = np.array([sp.beta.cdf(x=rv, a=10, b=10, loc=0, scale=1000) for rv in bids])

γ = np.linspace(-0.75, 1, num=100)

pibp_values = np.linspace(0, 900 + 1)

X, Y = np.meshgrid(γ, pibp_values)

Z = np.array(

[

[

bids[

np.argmax(

certainty_equivalent_values_calculator(

u=partial(u, γ=γ_i, a=0, b=1),

u_inv=partial(u_inv, γ=γ_i, a=0, b=1),

x=np.vstack((pibp - bids, np.zeros(bids.shape))).T,

p=np.vstack((p_acquire, 1 - p_acquire)).T,

γ=γ_i,

),

axis=1,

)[0]

]

for γ_i in γ

]

for pibp in pibp_values

]

)

# Plot the surface.

surf = ax.plot_surface(X, Y, Z, cmap=cm.coolwarm, linewidth=0, antialiased=False,)

ax.view_init(30, 40)

ax.set_xlabel(r"$\gamma$")

ax.set_ylabel(r"PIBP")

ax.set_zlabel("Optimal Bid Amount")

ax.set_title("Sensitivity Analysis of Optimal Bid Amount Vs. $\gamma$ and PIBP")

# Add a color bar which maps values to colors.

fig.colorbar(surf, shrink=0.5, aspect=5)

plt.show()

time: 39.2 s (started: 2021-04-02 15:45:01 +08:00)