Certain Equivalents and Sensitivity Analysis¶

By: Chengyi (Jeff) Chen

%load_ext autotime

%load_ext nb_black

%matplotlib notebook

%config InlineBackend.figure_format = 'retina'

# Graphing

import matplotlib.pyplot as plt

import seaborn as sns

# Plotting Design Configs

sns.set(

font="Verdana",

rc={

"axes.axisbelow": False,

"axes.edgecolor": "lightgrey",

"axes.facecolor": "None",

"axes.grid": True,

"grid.color": "lightgrey",

"axes.labelcolor": "dimgrey",

"axes.spines.right": False,

"axes.spines.top": False,

"figure.facecolor": "white",

"lines.solid_capstyle": "round",

"patch.edgecolor": "w",

"patch.force_edgecolor": True,

"text.color": "dimgrey",

"xtick.bottom": False,

"xtick.color": "dimgrey",

"xtick.direction": "out",

"xtick.top": False,

"ytick.color": "dimgrey",

"ytick.direction": "out",

"ytick.left": False,

"ytick.right": False,

"figure.dpi": 100,

"figure.figsize": (8, 6),

},

)

sns.set_context(

"notebook", rc={"font.size": 10, "axes.titlesize": 12, "axes.labelsize": 10}

)

sns.color_palette(palette="Spectral")

# General

import numpy as np

import scipy.stats as sp

import pandas as pd

from functools import partial

time: 864 ms (started: 2021-03-26 18:57:59 +08:00)

def ρ(γ):

"""Risk tolerance"""

return 1 / γ

time: 294 µs (started: 2021-03-26 18:57:59 +08:00)

def r(γ):

"""Risk Odds"""

return np.log(γ)

time: 280 µs (started: 2021-03-26 18:57:59 +08:00)

def u(x, γ: np.array = np.array([0.0]), a: float = 0.0, b: float = 1.0):

"""Assuming user satisifies the Δ property,

calculates the U-values using either a

Piecewise Linear u = a + bx if γ = 0 (Risk-Neutral)

else Exponential u = a + be^(-xγ) U-curve U(x)

Args:

x (np.array): Payoffs of prospects matrix, Shape = (Number of deals, Number of prospects in each deal)

γ (np.array): Risk-aversion coefficients, Shape = (Number of different risk-aversion coefficients for sensitivity analysis), Default = 0.0 (Risk-neutral) [γ > 0: Risk-averse, γ < 0: Risk-seeking]

a (float): Constant for U-curve

b (float): Coefficient for payoff variable

Returns:

np.array:

U-values, Shape = (Number of Risk Aversion Coefficients γ, Number of deals, Number of prospects in each deal)

"""

assert (

x.ndim == 2

), "Payoffs require 2 dimensions, first dim is number of deals, second is number of prospects in each deal."

γ = np.array([γ]) if np.isscalar(γ) else np.array(γ)

return np.array(

[

np.apply_along_axis(

func1d=lambda x, γ=γ: a + b * x if γ == 0 else a + b * np.exp(-x * γ),

axis=-1,

arr=x,

γ=γ_i,

)

for γ_i in γ

]

)

time: 597 µs (started: 2021-03-26 18:57:59 +08:00)

def eu(u, p):

"""Assuming user satisifies the Δ property, calculates the

hadamard product of the u values matrix and probabilities

matrix (respective probabilities associated with each

prospect in the u matrix)

Args:

u (np.array): U-values matrix, Shape = (Number of Risk Aversion Coefficients γ, Number of deals, Number of prospects in each deal)

p (np.array): Probabilities of each prospect matrix, Shape = (Number of Risk Aversion Coefficients γ, Number of deals, Number of prospects in each deal)

Returns:

np.array:

E-values, Shape = (Number of Risk Aversion Coefficients γ, Number of deals)

"""

assert (

u.shape == p.shape

), "U-values matrix must be the same shape as the probabilities matrix."

assert (

u.ndim == 3

), "Both matrices must have 3 dimensions, Shape = (Number of Risk Aversion Coefficients γ, Number of deals, Number of prospects in each deal)."

return np.sum(u * p, axis=-1)

time: 473 µs (started: 2021-03-26 18:57:59 +08:00)

def u_inv(eu, γ: np.array = np.array([0.0]), a: float = 0, b: float = 1):

"""Piecewise Inverse of Linear if γ = 0 (Risk-Neutral)

else Inverse of Exponential U-curve Certain equivalent

function U^{-1}(x)

Args:

eu (np.array): E[U-Values] / Expectation over u-values, AKA E-values, Shape = (Number of Risk Aversion Coefficients γ, Number of deals)

γ (np.array): Risk-aversion coefficients, Shape = (Number of different risk-aversion coefficients for sensitivity analysis), Default = 0.0 (Risk-neutral) [γ > 0: Risk-averse, γ < 0: Risk-seeking]

a (float): Constant for U-curve

b (float): Coefficient for payoff variable

Returns:

np.array:

Certainty Equivalent values, Shape = (Number of Risk Aversion Coefficients γ, Number of deals)

"""

γ = np.array([γ]) if np.isscalar(γ) else np.array(γ)

for eu_i, γ_i in zip(eu, γ):

if not np.isclose(γ_i, 0):

assert np.alltrue(

eu_i > 0

), "E[U-Values] / Expectation over u-values must be positive for γ > 0 and γ < 0 in order for inverse of Exponential U-curve to work."

assert (

eu.shape[0] == γ.shape[0]

), "E-values first dimension must be the same as γ first dimension for inverse operation."

return np.array(

[

list(

map(

lambda eu, γ=γ_i: (eu - a) / b if γ == 0 else -(1 / γ) * np.log(eu),

eu_i,

)

)

for eu_i, γ_i in zip(eu, γ)

]

)

time: 819 µs (started: 2021-03-26 18:58:00 +08:00)

def certainty_equivalent_values_calculator(

u,

u_inv,

x: np.array = None,

p: np.array = None,

N: int = 10,

payout_lb: float = 0.0,

payout_ub: float = 100.0,

γ: np.array = np.array([0.0]),

):

"""Assuming user satisifies the Δ property, calculates the Certainty Equivalent values for a given

payoff matrix `x` and probability matrix `p`. If both matrices

are not provided, random matrices will be sampled to simulate

calculations.

Args:

u (function): U-curve function

u_inv (function): Inverse U-curve function

x (np.array): Payoffs of prospects matrix, Shape = (Number of deals, Number of prospects in each deal)

p (np.array): Probabilities of each prospect matrix, Shape = (Number of deals, Number of prospects in each deal)

N (int): Number of prospects

payout_lb (float): Lower Bound of Payout for simulation, Default = 0.0

payout_ub (float): Upper Bound of Payout for simulation, Default = 100.0

γ (np.array): Risk-aversion coefficients, Shape = (Number of different risk-aversion coefficients for sensitivity analysis), Default = 0.0 (Risk-neutral) [γ > 0: Risk-averse, γ < 0: Risk-seeking]

Returns:

np.array:

Certainty Equivalent values, Shape = (Number of Risk Aversion Coefficients γ, Number of deals)

"""

γ = np.array([γ]) if np.isscalar(γ) else np.array(γ)

# Case 1: Simulator - Both x and p arent provided

if p is None and x is None:

# Preferential probabilities for each prospect

p = np.random.dirichlet(np.ones(N), size=1)

# Payouts for each prospect

x = np.expand_dims(np.random.randint(payout_lb, payout_ub, size=N), axis=0)

# Case 2: Simulator - Only payouts provided

elif p is None:

# Payouts for each prospect

x = np.expand_dims(

np.random.randint(payout_lb, payout_ub, size=p.shape[-1]), axis=0

)

# Case 3: Simulator - Only probabilities provided

elif x is None:

# Preferential probabilities for each prospect

p = np.random.dirichlet(np.ones(x.shape[-1]), size=1)

# Case 4: Calculator - Both are provided

else:

pass

# Check that payoffs and probability assignments are the same shape

assert (

x.shape == p.shape

), "Payoffs `x` and Probabilities `p` must be the same shape=(Number of deals, Number of prospects in each deal)."

# Calculates U-values Shape = (Number of Risk Aversion Coefficients γ, Number of deals, Number of prospects in each deal)

u_values = u(x, γ=γ)

# Reshape p to match U-values shape

p_reshaped = np.array([p for _ in range(u_values.shape[0])])

# Expectation of U values Shape = (Number of Risk Aversion Coefficients γ, Number of deals)

eu_values = eu(u=u_values, p=p_reshaped)

# Certainty equivalent value of deal

ce_values = u_inv(eu_values, γ=γ)

return ce_values

time: 958 µs (started: 2021-03-26 18:58:00 +08:00)

1) Simple Certain Equivalent Calculator¶

Build a certain equivalent calculator for a decision maker with an exponential u-curve facing a deal with 5 possible prospects with pay-offs. Build a model that allows a sensitivity analysis to the risk aversion coefficient.

# Number of prospects

N = 5

# Risk-aversion coefficient

γ = np.linspace(-1, 1, num=100)

fig, ax = plt.subplots(1, 1)

ax.plot(

γ,

certainty_equivalent_values_calculator(

u, u_inv, N=5, payout_lb=0, payout_ub=100, γ=γ

),

)

ax.set_xlabel("γ")

ax.set_ylabel("CE")

ax.set_title("CE(Decision Maker)")

plt.show()

time: 35.4 ms (started: 2021-03-26 18:58:00 +08:00)

2) 1000-degree Certain Equivalent Calculator¶

Build a certain equivalent calculator for a decision maker with an exponential u-curve facing a deal represented by a

Discretized Uniform distribution on the range 1 ~ 1000

# Number of prospects

N = 100

# Payouts for each prospect

x = np.expand_dims(

np.array([sp.uniform.rvs(loc=0, scale=1000) for _ in range(N)]), axis=0

)

# Preferential probabilities for each prospect

p = np.array([sp.uniform.pdf(x=rv, loc=0, scale=1000) for rv in x])

# Risk-aversion coefficient

γ = np.linspace(-1, 1, num=100)

fig, ax = plt.subplots(1, 1)

ax.plot(

γ,

certainty_equivalent_values_calculator(

u, u_inv, x, p, N, payout_lb=None, payout_ub=None, γ=γ

),

)

ax.set_xlabel("γ")

ax.set_ylabel("CE")

ax.set_title(r"CE(Decision Maker) with $p(X) \sim U(0, 1000)$")

plt.show()

time: 34.4 ms (started: 2021-03-26 18:58:00 +08:00)

<ipython-input-4-9a6997586247>:24: RuntimeWarning: overflow encountered in exp

func1d=lambda x, γ=γ: a + b * x if γ == 0 else a + b * np.exp(-x * γ),

Discretized Beta distribution on the range 1 ~ 1000

# Number of prospects

N = 100

# Preferential probabilities for each prospect

x = np.expand_dims(

np.array([sp.beta.rvs(a=2, b=2, loc=0, scale=1000) for _ in range(N)]), axis=0

)

# Payouts for each prospect

p = np.array([sp.beta.pdf(x=rv, a=2, b=2, loc=0, scale=1000) for rv in x])

# Risk-aversion coefficient

γ = np.linspace(-1, 1, num=100)

fig, ax = plt.subplots(1, 1)

ax.plot(

γ,

certainty_equivalent_values_calculator(

u, u_inv, x, p, N, payout_lb=None, payout_ub=None, γ=γ

),

)

ax.set_xlabel("γ")

ax.set_ylabel("CE")

ax.set_title(r"CE(Decision Maker) with $p(X) \sim Beta(a=2, b=2, 0, 1000)$")

plt.show()

time: 40.4 ms (started: 2021-03-26 18:58:00 +08:00)

<ipython-input-4-9a6997586247>:24: RuntimeWarning: overflow encountered in exp

func1d=lambda x, γ=γ: a + b * x if γ == 0 else a + b * np.exp(-x * γ),

3) Heat Maps: Probability vs Severity Plots¶

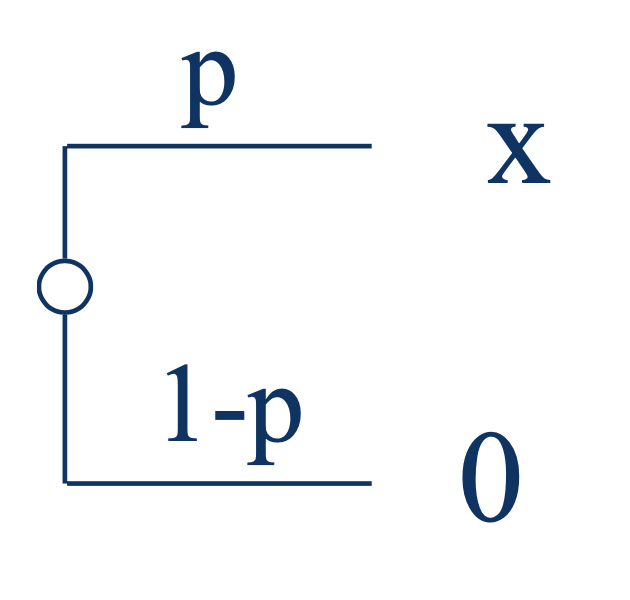

Assuming a Risk-Neutral decision maker, and starting with a deal that has a 0.9 probability of losing \(\$1\) Million and a 0.1 probability of a zero pay-off, find the value of \(X\) in the following deals that makes you indifferent to this deal.

Let \(u(x, \gamma) = e^{-x\gamma} \) and \(u^{-1}(u, \gamma) = x = -\frac{1}{\gamma}\ln u\) be the \(u\)-value function and it’s inverse.

Let \(N, M\) be the number of prospects in deal \(A\) and \(B\) respectively.

Let \(p^{(A)} \in \mathbb{R}^N: \mathbb{1}^\top p^{(A)} = 1\) and \(p^{(B)} \in \mathbb{R}^M: \mathbb{1}^\top p^{(B)} = 1\) be the vector of probabilities of getting different prospects \(a\), \(b\), for deals \(A\) and \(B\) respectively:

b_j = lambda a, p_A, b_excl_j, p_B_excl_j, p_B_j, γ=0: u_inv(

(np.sum(u(a, γ=γ) * p_A, axis=-1) - np.sum(u(b_excl_j, γ=γ) * p_B_excl_j, axis=-1))

/ p_B_j,

γ=γ,

)

time: 1.25 ms (started: 2021-03-26 18:58:00 +08:00)

a) A Deal with 0.8 Probability of \(X\) and 0.2 Probability of Zero

b_j(

a=np.array([[-1e6, 0]]),

p_A=np.array([[0.9, 0.1]]),

b_excl_j=np.array([[0]]),

p_B_excl_j=np.array([[0.2]]),

p_B_j=np.array([[0.8]]),

)[0][0]

-1125000.0

time: 3.24 ms (started: 2021-03-26 18:58:00 +08:00)

b) A Deal with 0.7 Probability of \(X\) and 0.3 Probability of Zero

b_j(

a=np.array([[-1e6, 0]]),

p_A=np.array([[0.9, 0.1]]),

b_excl_j=np.array([[0]]),

p_B_excl_j=np.array([[0.3]]),

p_B_j=np.array([[0.7]]),

)[0][0]

-1285714.2857142857

time: 3.54 ms (started: 2021-03-26 18:58:00 +08:00)

c) A Deal with 0.6 Probability of \(X\) and 0.4 Probability of Zero

b_j(

a=np.array([[-1e6, 0]]),

p_A=np.array([[0.9, 0.1]]),

b_excl_j=np.array([[0]]),

p_B_excl_j=np.array([[0.4]]),

p_B_j=np.array([[0.6]]),

)[0][0]

-1500000.0

time: 3.91 ms (started: 2021-03-26 18:58:00 +08:00)

d) A Deal with 0.5 Probability of \(X\) and 0.5 Probability of Zero

b_j(

a=np.array([[-1e6, 0]]),

p_A=np.array([[0.9, 0.1]]),

b_excl_j=np.array([[0]]),

p_B_excl_j=np.array([[0.5]]),

p_B_j=np.array([[0.5]]),

)[0][0]

-1800000.0

time: 3.37 ms (started: 2021-03-26 18:58:00 +08:00)

e) A Deal with 0.4 Probability of \(X\) and 0.6 Probability of Zero

b_j(

a=np.array([[-1e6, 0]]),

p_A=np.array([[0.9, 0.1]]),

b_excl_j=np.array([[0]]),

p_B_excl_j=np.array([[0.6]]),

p_B_j=np.array([[0.4]]),

)[0][0]

-2250000.0

time: 2.96 ms (started: 2021-03-26 18:58:00 +08:00)

f) A Deal with 0.3 Probability of \(X\) and 0.7 Probability of Zero

b_j(

a=np.array([[-1e6, 0]]),

p_A=np.array([[0.9, 0.1]]),

b_excl_j=np.array([[0]]),

p_B_excl_j=np.array([[0.7]]),

p_B_j=np.array([[0.3]]),

)[0][0]

-3000000.0

time: 3.16 ms (started: 2021-03-26 18:58:00 +08:00)

g) A Deal with 0.2 Probability of \(X\) and 0.8 Probability of Zero

b_j(

a=np.array([[-1e6, 0]]),

p_A=np.array([[0.9, 0.1]]),

b_excl_j=np.array([[0]]),

p_B_excl_j=np.array([[0.8]]),

p_B_j=np.array([[0.2]]),

)[0][0]

-4500000.0

time: 3.17 ms (started: 2021-03-26 18:58:00 +08:00)

h) A Deal with 0.1 Probability of \(X\) and 0.9 Probability of Zero

b_j(

a=np.array([[-1e6, 0]]),

p_A=np.array([[0.9, 0.1]]),

b_excl_j=np.array([[0]]),

p_B_excl_j=np.array([[0.9]]),

p_B_j=np.array([[0.1]]),

)[0][0]

-9000000.0

time: 2.98 ms (started: 2021-03-26 18:58:00 +08:00)

Plot the (Probability of \(X\)) vs. \(X\).

fig, ax = plt.subplots(1, 1)

ax.plot(

np.array(

[

b_j(

a=np.array([[-1e6, 0]]),

p_A=np.array([[0.9, 0.1]]),

b_excl_j=np.array([[0]]),

p_B_excl_j=np.array([[1 - p_B_j]]),

p_B_j=np.array([[p_B_j]]),

)[0][0]

for p_B_j in np.linspace(0.01, 0.99, num=100)

]

),

np.linspace(0.01, 0.99, num=100),

label="γ = 0",

)

ax.set_xlabel(r"$X$")

ax.set_ylabel(r"$p(X)$")

ax.set_title(r"$p(X)$ Vs. $X$ Heat Map for Risk-Neutral (γ=0) Decision Maker")

plt.show()

time: 55.4 ms (started: 2021-03-26 18:58:00 +08:00)

Repeat for a decision maker with a Risk Aversion Coefficient of \(10^{-6}\).

fig, ax = plt.subplots(1, 1)

ax.plot(

np.array(

[

b_j(

a=np.array([[-1e6, 0]]),

p_A=np.array([[0.9, 0.1]]),

b_excl_j=np.array([[0]]),

p_B_excl_j=np.array([[1 - p_B_j]]),

p_B_j=np.array([[p_B_j]]),

γ=0,

)[0][0]

for p_B_j in np.linspace(0.01, 0.99, num=100)

]

),

np.linspace(0.01, 0.99, num=100),

label="γ = 0",

)

ax.plot(

np.array(

[

b_j(

a=np.array([[-1e6, 0]]),

p_A=np.array([[0.9, 0.1]]),

b_excl_j=np.array([[0]]),

p_B_excl_j=np.array([[1 - p_B_j]]),

p_B_j=np.array([[p_B_j]]),

γ=1e-06,

)[0]

for p_B_j in np.linspace(0.01, 0.99, num=100)

]

),

np.linspace(0.01, 0.99, num=100),

label="γ = 10^-6",

)

ax.set_xlabel(r"$X$")

ax.set_ylabel(r"$p(X)$")

ax.set_title(

r"$p(X)$ Vs. $X$ Heat Map for Risk-Neutral (γ = 0) and Risk-Averse (γ = 10^-6) Decision Maker"

)

plt.legend()

plt.show()

time: 86.5 ms (started: 2021-03-26 18:58:00 +08:00)

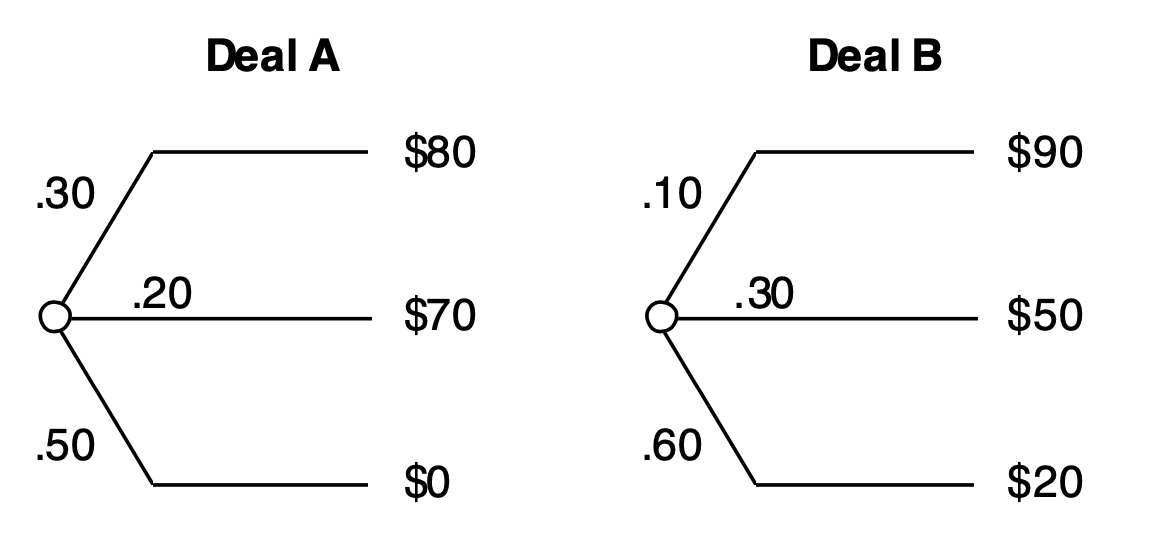

4) Risk-Sensitivity Profile¶

Plot the Risk Sensitivity profile for the following two deals.

The Risk-Sensitivity profile is a plot of the certain equivalent of a deal vs, the risk aversion coefficient, \(\gamma\). Draw the plot from \(\gamma = −1\) to \(\gamma = +1\)

# Risk-aversion coefficient

γ = np.linspace(-1, 1, num=100)

fig, ax = plt.subplots(1, 1)

ax.plot(

γ,

certainty_equivalent_values_calculator(

u,

u_inv,

np.array([[80, 70, 0]]),

np.array([[0.3, 0.2, 0.5]]),

N,

payout_lb=None,

payout_ub=None,

γ=γ,

),

label=r"CE(Deal A)",

)

ax.plot(

γ,

certainty_equivalent_values_calculator(

u,

u_inv,

np.array([[90, 50, 20]]),

np.array([[0.1, 0.3, 0.6]]),

N,

payout_lb=None,

payout_ub=None,

γ=γ,

),

label=r"CE(Deal B)",

)

ax.set_xlabel("γ")

ax.set_ylabel("CE")

ax.set_title("Risk Sensitivity Profile for Deal A and B")

plt.legend()

plt.show()

time: 43 ms (started: 2021-03-26 18:58:00 +08:00)

5) Large Monetary Prospects Using an Exponential U-Curve¶

In the deal below, assume \(p = 0.5\) and a decision maker with an exponential u-curve and a risk-aversion coefficient \(\gamma = 0.001\). I.e. the equation for the u-curve is

Plot the certain equivalent of the deal vs. \(X\) for the range where \(X=\$0\) to \(X=\$10,000\) in increments of \({\$500}\).

Explain and interpret the results.

# Preferential probabilities for each prospect

x = np.array(

list(zip(np.arange(0, 1e4 + 1, 500), np.zeros(len(np.arange(0, 1e4 + 1, 500)))))

)

# Payouts for each prospect

p = np.array([[0.5, 0.5] for _ in x])

# Risk-aversion coefficient

γ = np.array([0, 0.001, -0.001])

fig, ax = plt.subplots(1, 1)

ax.plot(

x[:, 0],

certainty_equivalent_values_calculator(

u, u_inv, x, p, N=None, payout_lb=None, payout_ub=None, γ=γ

)[0],

label="γ = 0 (Risk-Neutral Individual)",

)

ax.plot(

x[:, 0],

certainty_equivalent_values_calculator(

u, u_inv, x, p, N=None, payout_lb=None, payout_ub=None, γ=γ

)[1],

label="γ = 0.001 (Risk-Averse Individual)",

)

ax.plot(

x[:, 0],

certainty_equivalent_values_calculator(

u, u_inv, x, p, N=None, payout_lb=None, payout_ub=None, γ=γ

)[2],

label="γ = -0.001 (Risk-Seeking Individual)",

)

ax.set_xlabel(r"$X$")

ax.set_ylabel("CE")

ax.set_title(

r"CE(Decision Maker) $U(X) = a + be^{-\gamma x}$, $a = 0, b = 1$ Vs. $X$(\$)"

)

plt.legend()

plt.show()

time: 33.3 ms (started: 2021-03-26 18:58:00 +08:00)

We notice that the risk-averse individual (\(\gamma = 0.001 > 0\))’s certainty equivalent value for all gambles are lower than the risk-neutral individual (\(\gamma = 0\)), and much lower than the risk-seeking individual (\(\gamma = -0.001 < 0\)). For example, when presented with a deal to win \(\$4,000\) or nothing with equal probability, the risk-neutral individual is indifferent to playing the deal or simply getting the traditional expected value of \(\mathbb{E}\left[X\right] = \$2,000.00\). The risk-averse individual will be indifferent to that deal or getting \(\$675.00\) while the risk-seeking individual will be indifferent to that deal or getting \(\$3,325.00\).

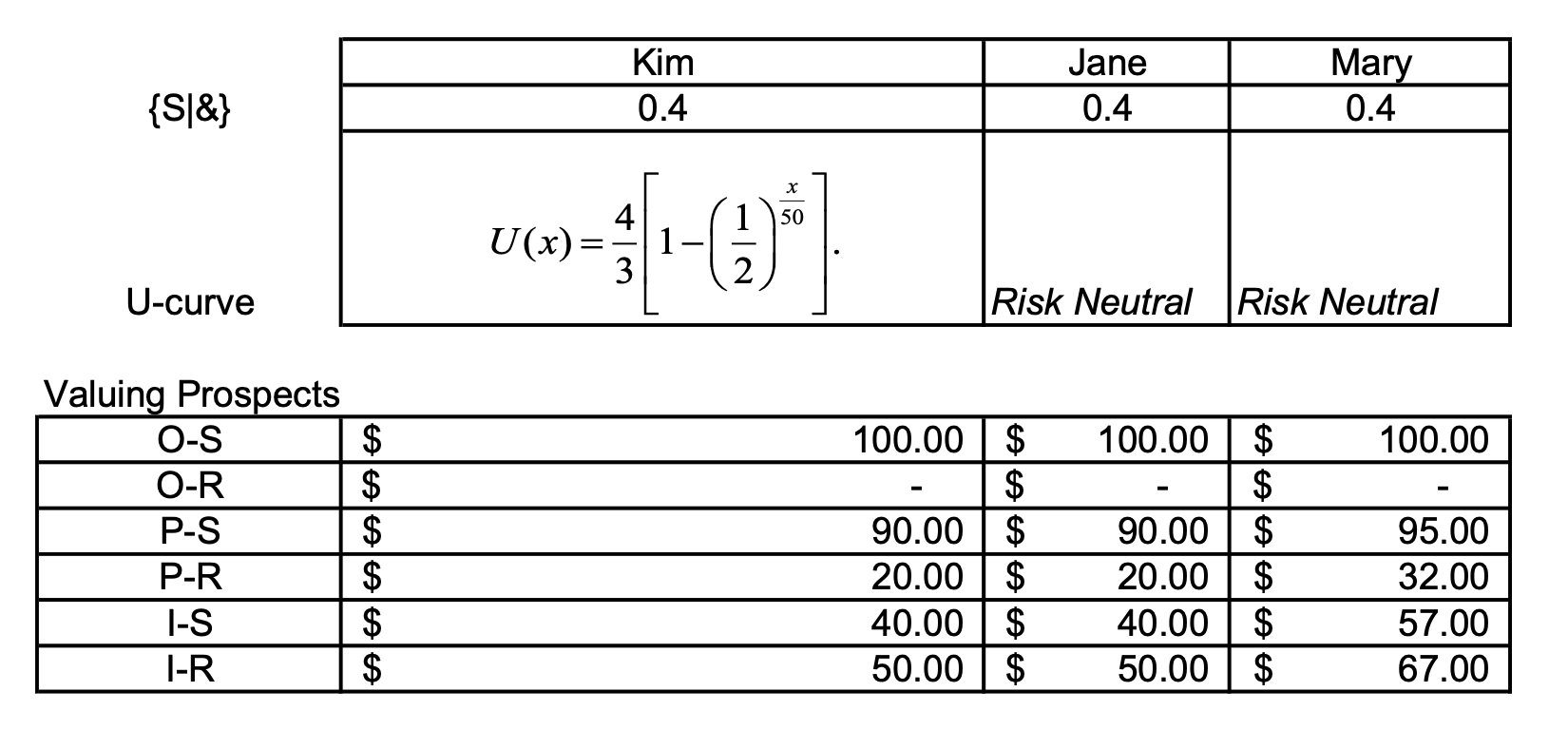

6) EXTRA CREDIT: Sensitivity to Value of Clairvoyance¶

In the party problem, the following table represents the probabilities, prospects, and \(u\)-values for Kim, Mary, and Jane.

a) Kim’s risk Odd for \(\$50\) are \(r_{50} = 2 :1\). What is her risk tolerance?

Assuming that Kim satisfies the \(\Delta\) property,

Also, we can find her risk tolerance by comparing the forms of the exponential \(U\)-curves:

b) Build a spreadsheet to calculate the Value of Clairvoyance for each person.

Assuming a person satisfies the \(\Delta\) property,

def value_of_clairvoyance(u, u_inv, x, p):

"""Calculates the Value of Clairvoyance

= Value of Free Clairvoyance - Value of No Clairvoyance

AKA How much more value we get when we have access

to an oracle that can tell us the actual outcome of a

random event.

Args:

u (function): U-curve function

u_inv (function): Inverse U-curve function

x (np.array): Payoffs of prospects matrix, Shape = (Number of deals, Number of prospects in each deal)

p (np.array): Probabilities of each prospect matrix, Shape = (Number of deals, Number of prospects in each deal)

Returns:

float:

Value of the Clairvoyance

"""

# Check that payoffs and probability assignments are the same shape

assert (

x.shape == p.shape

), "Payoffs `x` and Probabilities `p` must be the same shape=(Number of deals, Number of prospects in each deal)."

# Value of Free Clairvoyance

vfc = certainty_equivalent_values_calculator(

u=u,

u_inv=u_inv,

x=np.array([x.max(axis=0)]),

p=np.array([p[np.argmax(x, axis=0), np.array(range(x.shape[1]))]]),

γ=np.array([u.keywords["γ"]]),

)[0][0]

# Value of No Clairvoyance

vnc = np.max(

certainty_equivalent_values_calculator(

u=u, u_inv=u_inv, x=x, p=p, γ=np.array([u.keywords["γ"]]),

)

)

# Value of Clairvoyance

return np.round(vfc - vnc, 2)

time: 2 ms (started: 2021-03-26 18:58:00 +08:00)

Kim’s Value of Clairvoyance

# Probabilities of Sun and Rain

p = np.array([[0.4, 0.6]])

# Prospect Valuation

x_kim = pd.DataFrame(

np.array([[100, 90, 40], [0, 20, 50]]),

index=["Sun", "Rain"],

columns=["Outdoors", "Porch", "Indoors"],

)

value_of_clairvoyance(

u=partial(u, γ=np.log(2) / 50, a=4 / 3, b=-4 / 3),

u_inv=partial(u_inv, γ=np.log(2) / 50, a=4 / 3, b=-4 / 3),

x=x_kim.T.values,

p=np.repeat(p, repeats=x_kim.T.shape[0], axis=0),

)

-50.0

time: 6.39 ms (started: 2021-03-26 18:58:00 +08:00)

Jane’s Value of Clairvoyance

# Probabilities of Sun and Rain

p = np.array([[0.4, 0.6]])

# Prospect Valuation

x_jane = pd.DataFrame(

np.array([[100, 90, 40], [0, 20, 50]]),

index=["Sun", "Rain"],

columns=["Outdoors", "Porch", "Indoors"],

)

value_of_clairvoyance(

u=partial(u, γ=0, a=0, b=1),

u_inv=partial(u_inv, γ=0, a=0, b=1),

x=x_jane.T.values,

p=np.repeat(p, repeats=x_jane.T.shape[0], axis=0),

)

22.0

time: 7.24 ms (started: 2021-03-26 18:58:00 +08:00)

Mary’s Value of Clairvoyance

# Probabilities of Sun and Rain

p = np.array([[0.4, 0.6]])

# Prospect Valuation

x_mary = pd.DataFrame(

np.array([[100, 95, 57], [0, 32, 67]]),

index=["Sun", "Rain"],

columns=["Outdoors", "Porch", "Indoors"],

)

value_of_clairvoyance(

u=partial(u, γ=0, a=0, b=1),

u_inv=partial(u_inv, γ=0, a=0, b=1),

x=x_mary.T.values,

p=np.repeat(p, repeats=x_mary.T.shape[0], axis=0),

)

17.2

time: 8.09 ms (started: 2021-03-26 18:58:00 +08:00)

c) Conduct a sensitivity analysis of the Value of Clairvoyance to the probability of Sun for each person and plot the three-curves on one graph.

# Range of P(Sun) values to perform sensitivity analysis of VOC over

p_sun_values = np.linspace(0.001, 0.999, num=100)

# VOC values for each P(Sun) value

kim_voc_values, jane_voc_values, mary_voc_values = [

[

value_of_clairvoyance(

u=u,

u_inv=u_inv,

x=x,

p=np.repeat(np.array([[p_sun, 1 - p_sun]]), repeats=x.shape[0], axis=0),

)

for p_sun in p_sun_values

]

for u, u_inv, x in [

[

partial(u, γ=np.log(2) / 50, a=4 / 3, b=-4 / 3),

partial(u_inv, γ=np.log(2) / 50, a=4 / 3, b=-4 / 3),

x_kim.T.values,

],

[partial(u, γ=0, a=0, b=1), partial(u_inv, γ=0, a=0, b=1), x_jane.T.values],

[partial(u, γ=0, a=0, b=1), partial(u_inv, γ=0, a=0, b=1), x_mary.T.values],

]

]

fig, ax = plt.subplots(1, 1)

ax.plot(

p_sun_values, kim_voc_values, label="Kim",

)

ax.plot(

p_sun_values, jane_voc_values, label="Jane",

)

ax.plot(

p_sun_values, mary_voc_values, label="Mary",

)

ax.set_xlabel(r"$p(Sun)$")

ax.set_ylabel("Value of Clairvoyance")

ax.set_title(r"Value of Clairvoyance Vs. $p(Sun)$")

plt.legend()

plt.show()

time: 188 ms (started: 2021-03-26 18:58:00 +08:00)

d) Conduct a sensitivity analysis of VOC to both probability of Sun and the risk aversion coefficient for Kim.

from mpl_toolkits.mplot3d import Axes3D

from matplotlib import cm, colors

from matplotlib.ticker import LinearLocator

fig, ax = plt.subplots(subplot_kw={"projection": "3d"})

# Because EU values need to be positive for

# the inverse of an exponential to be defined,

# Kim's U-curve demands that γ values should

# be chosen such that e^{-xγ} <= 1. Hence, we wil

# only perfrom sensitivity analysis over γ > 0

γ = np.linspace(0.0001, 0.0099, num=100)

X, Y = np.meshgrid(p_sun_values, γ)

Z = np.array(

[

[

value_of_clairvoyance(

u=partial(u, γ=γ_i, a=4 / 3, b=-4 / 3),

u_inv=partial(u_inv, γ=γ_i, a=4 / 3, b=-4 / 3),

x=x_kim.T.values,

p=np.repeat(

np.array([[p_sun, 1 - p_sun]]), repeats=x_kim.T.shape[0], axis=0

),

)

for p_sun in p_sun_values

]

for γ_i in γ

]

)

# Plot the surface.

surf = ax.plot_surface(X, Y, Z, cmap=cm.coolwarm, linewidth=0, antialiased=False,)

ax.set_xlabel(r"$p(Sun)$")

ax.set_ylabel(r"Risk-aversion Coefficient $\gamma$")

ax.set_zlabel("VOC")

ax.set_title("Sensitivity Analysis of Value of Clairvoyance (VOC)")

# Add a color bar which maps values to colors.

fig.colorbar(surf, shrink=0.5, aspect=5)

plt.show()

time: 8.56 s (started: 2021-03-26 18:58:01 +08:00)